Recall: The Firm's Two Problems

- 1st Stage: firm's profit maximization problem:

Choose: < output >

In order to maximize: < profits >

We'll cover this later...first we'll explore:

2nd Stage: firm's cost minimization problem:

Choose: < inputs >

In order to minimize: < cost >

Subject to: < producing the optimal output >

- Minimizing costs ⟺ maximizing profits

A Competitive Market

- We assume (for now) the firm is in a competitive industry:

Firms’ products are perfect substitutes

Firms are “price-takers”, no one firm can affect the market price

Market entry and exit are free†

† Remember this feature. It turns out to be the most important feature that distinguishes different types of industries!

Profit

Recall that profit is is: π=pq⏟revenues−(wl+rk)⏟costs

We’ll first take a closer look at costs today, then at revenues

Next class we'll put them together to find q∗ that maximizes π (the first stage problem)

Costs in Economics are Opportunity Costs

- Remember, economic costs are different from common conception of "cost"

- Accounting cost: monetary cost

- Economic cost: value of next best alternative use of resources given up (i.e. opportunity cost)

Costs in Economics are Opportunity Costs

This leads to the difference between

- Accounting profit: revenues minus accounting costs

- Economic profit: revenues minues opportunity costs

One of the most difficult concepts to think about!

Costs in Economics are Opportunity Costs

Another helpful perspective:

Accounting cost: what you historically paid for a resource

Economic cost: what you can currently get in the market for a selling a resource

- Resource's value in alternative uses

Costs in Economics are Opportunity Costs

Because resources are scarce, and have rivalrous uses,

In functioning markets, the market price measures the opportunity cost of using a resource for an alternative use

Firms not only pay for direct use of a resource, but also indirectly for "pulling it out" of an alternate use in the economy!

Opportunity Costs in Production

- Every choice incurs an opportunity cost

Examples:

- If you choose to start a business, you may give up your salary at your current job

- If you invest in a factory, you give up other investment opportunities

- If you use an office building you own, you cannot rent it to other people

- If you hire a skilled worker, you must pay them a high enough salary to deter them from working for other firms

Opportunity Cost is Hard for People

Opportunity Costs vs. Sunk Costs

Opportunity cost is a forward-looking concept

Choices made in the past with non-recoverable costs are called sunk costs

Sunk costs should not enter into future decisions

Many people have difficulty letting go of unchangeable past decisions: sunk cost fallacy

Sunk Costs: Examples

Sunk Costs: Examples

Sunks Costs: Examples

The Sunk Cost Fallacy

Common Sunk Costs in Business

Licensing fees, long-term lease contracts

Specific capital (with no alternative use): uniforms, menus, signs

Research & Development spending

Advertising spending

The Accounting vs. Economic Point of View I

- Helpful to consider two points of view:

"Accounting point of view": are you taking in more cash than you are spending?

"Economic point of view": is your product you making the best social use of your resources (i.e. are there higher-valued uses of your resources you are keeping them away from)?

The Accounting vs. Economic Point of View II

Social implications: are consumers best off with you using scarce resources (with alternative uses!) to produce your current product?

Remember: this is an economics course, not a business course!

- What might be good/bad for one business might have bad/good consequences for society!

- e.g. monopoly vs. competition

Fixed vs. Variable costs: Examples

Example: Airlines

Fixed costs: the aicraft

Variable costs: getting one more customer in a seat

Fixed vs. Variable costs: Examples

Example: Car Factory

Fixed costs: the factory, machines in the factory

Variable costs: producing one more car

Fixed vs. Variable costs: Examples

Example: Starbucks

Fixed costs: the retail space

Variable costs: producing one more cup of coffee

Fixed vs. Sunk costs

Diff. between fixed vs. sunk costs?

Sunk costs are a type of fixed cost that are not avoidable or recoverable

Many fixed costs can be avoided or changed in the long run

Common fixed, but not sunk, costs:

- rent for office space, durable equipment, operating permits (that are renewed)

When deciding to stay in business, fixed costs matter, sunk costs do not!

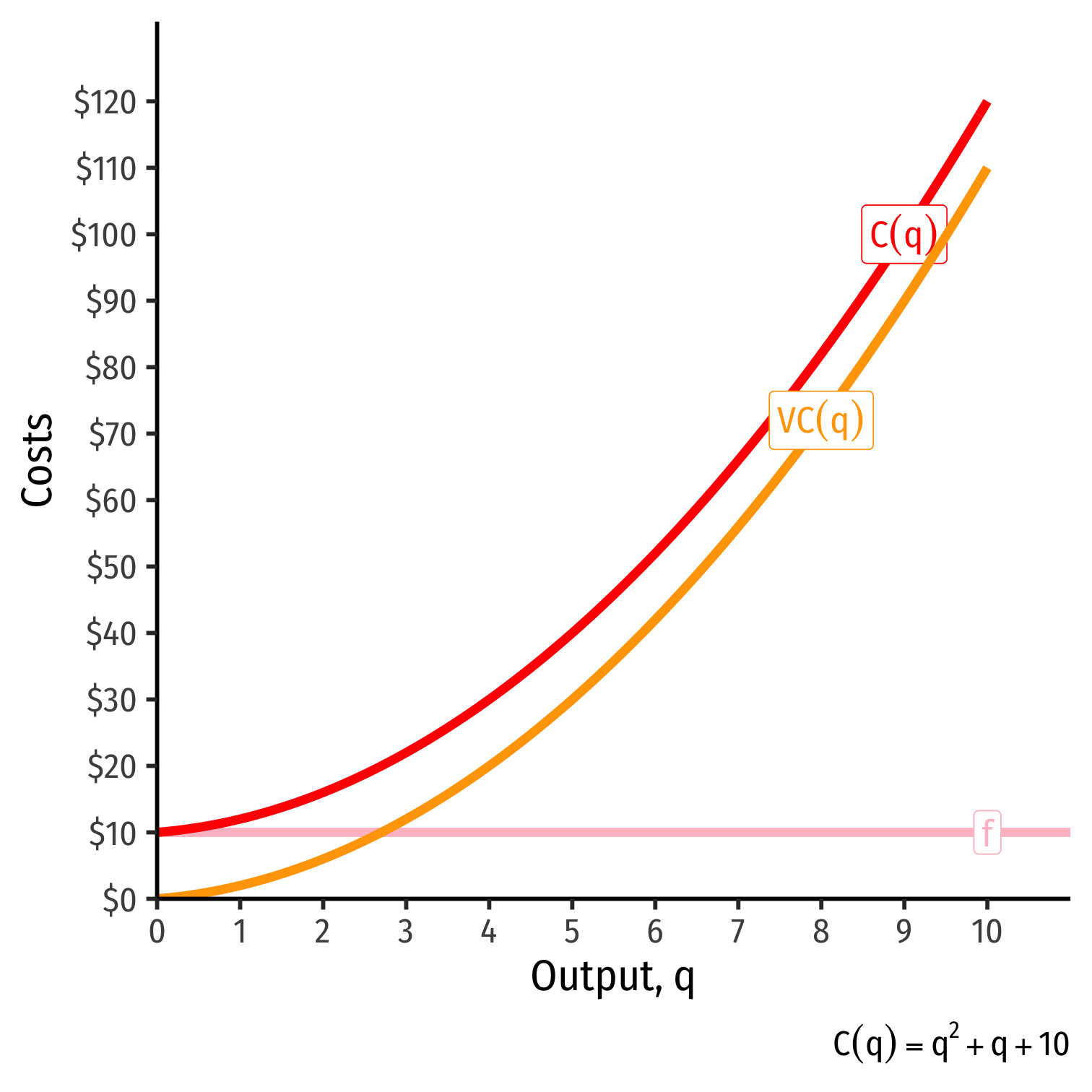

Cost Functions: Example, Visualized

| q | f | VC(q) | C(q) |

|---|---|---|---|

| 0 | 10 | 0 | 10 |

| 1 | 10 | 2 | 12 |

| 2 | 10 | 6 | 16 |

| 3 | 10 | 12 | 22 |

| 4 | 10 | 20 | 30 |

| 5 | 10 | 30 | 40 |

| 6 | 10 | 42 | 52 |

| 7 | 10 | 56 | 66 |

| 8 | 10 | 72 | 82 |

| 9 | 10 | 90 | 100 |

| 10 | 10 | 110 | 120 |

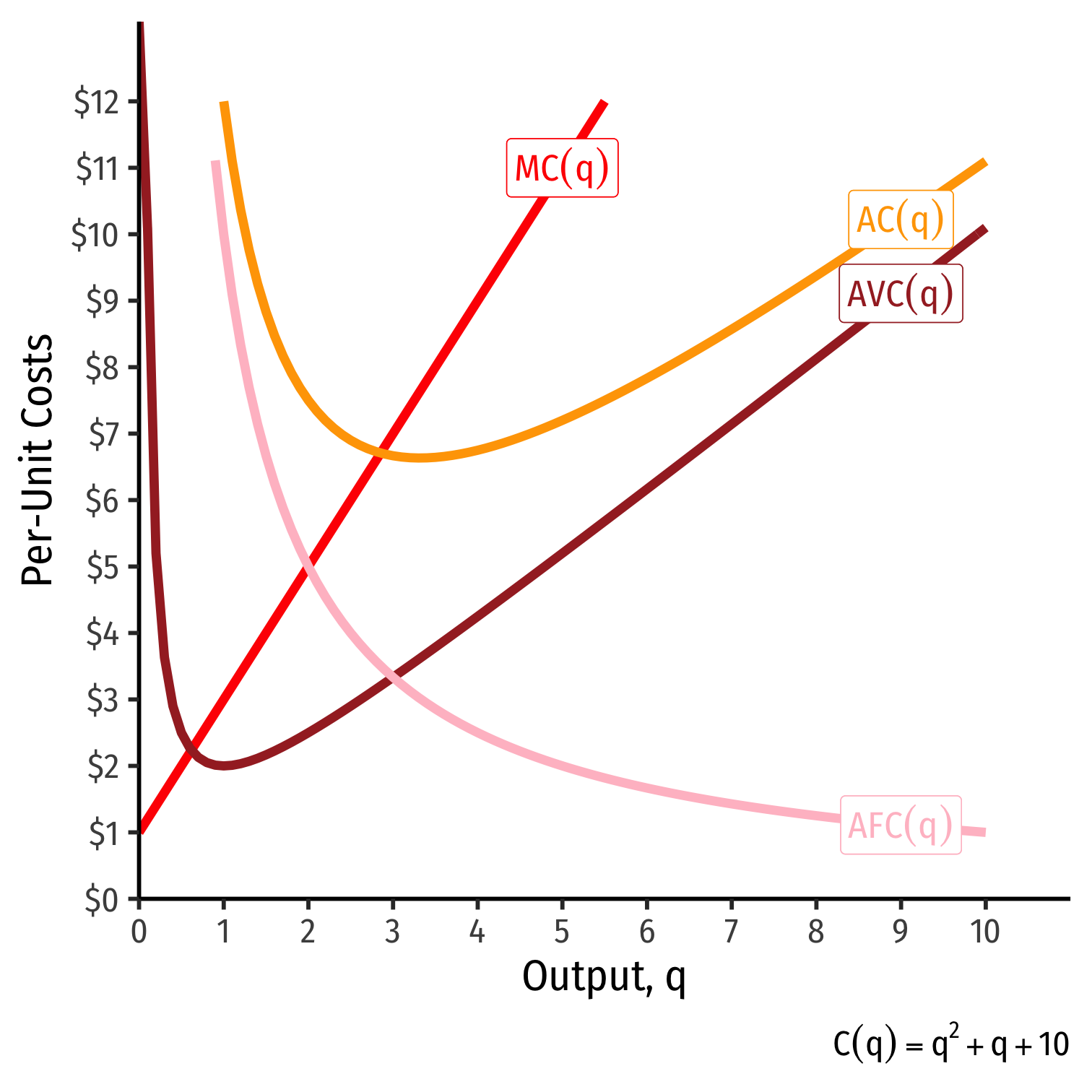

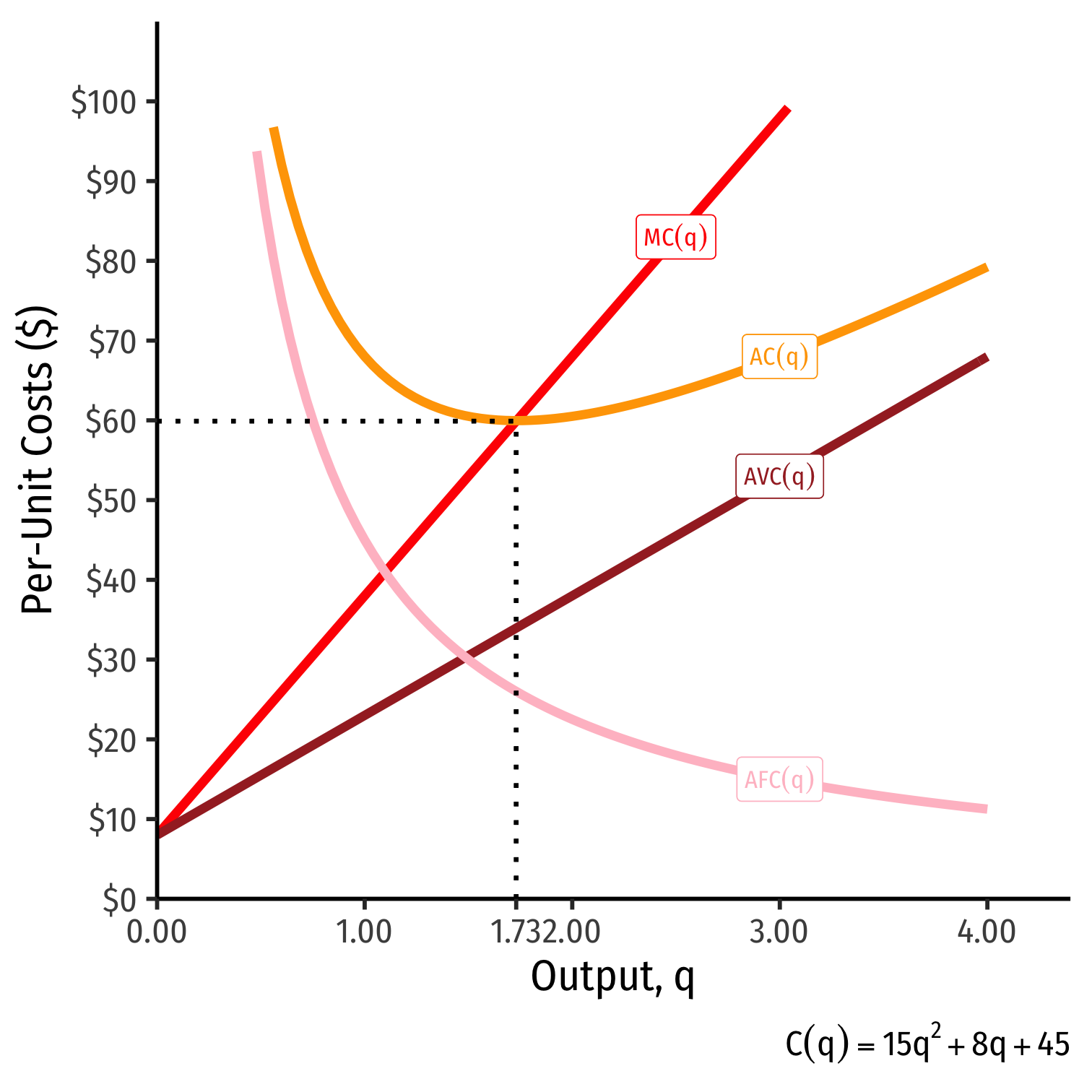

The Importance of Marginal Cost

Average and Marginal Costs: Visualized

| q | C(q) | MC(q) | AFC(q) | AVC(q) | AC(q) |

|---|---|---|---|---|---|

| 0 | 10 | − | − | − | − |

| 1 | 12 | 2 | 10.00 | 2 | 12.00 |

| 2 | 16 | 4 | 5.00 | 3 | 8.00 |

| 3 | 22 | 6 | 3.33 | 4 | 7.30 |

| 4 | 30 | 8 | 2.50 | 5 | 7.50 |

| 5 | 40 | 10 | 2.00 | 6 | 8.00 |

| 6 | 52 | 12 | 1.67 | 7 | 8.70 |

| 7 | 66 | 14 | 1.43 | 8 | 9.40 |

| 8 | 82 | 16 | 1.25 | 9 | 10.25 |

| 9 | 100 | 18 | 1.11 | 10 | 11.10 |

| 10 | 120 | 20 | 1.00 | 11 | 12.00 |

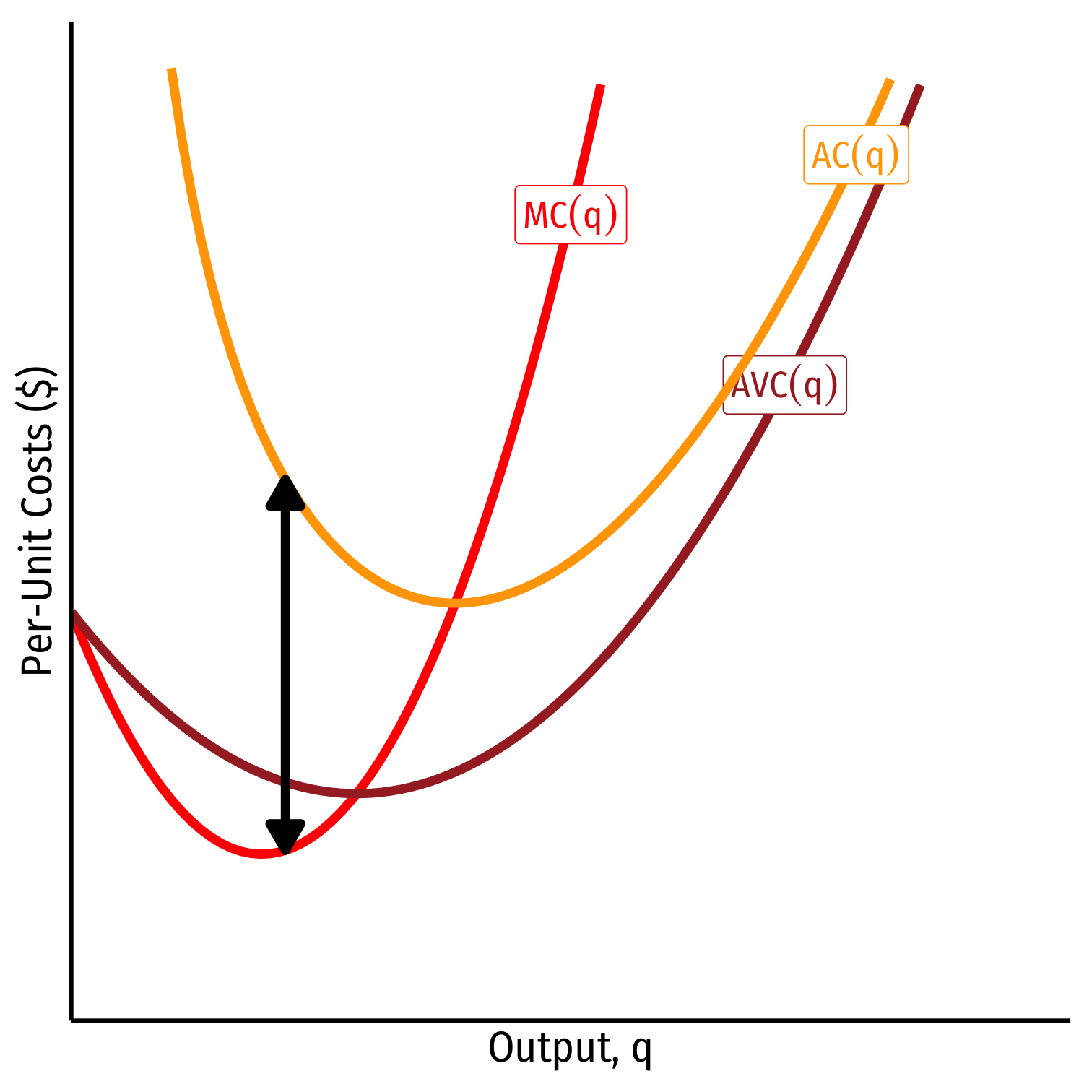

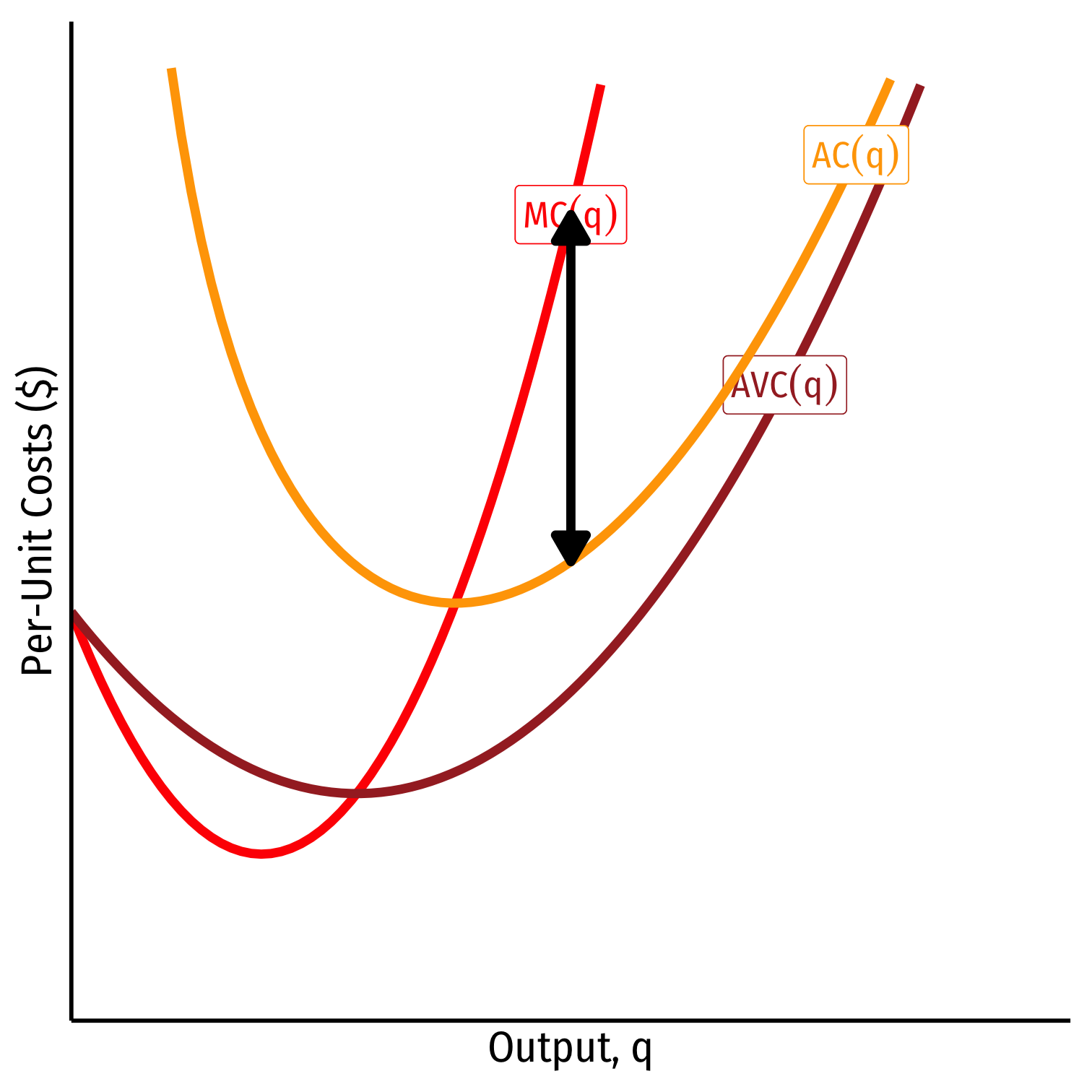

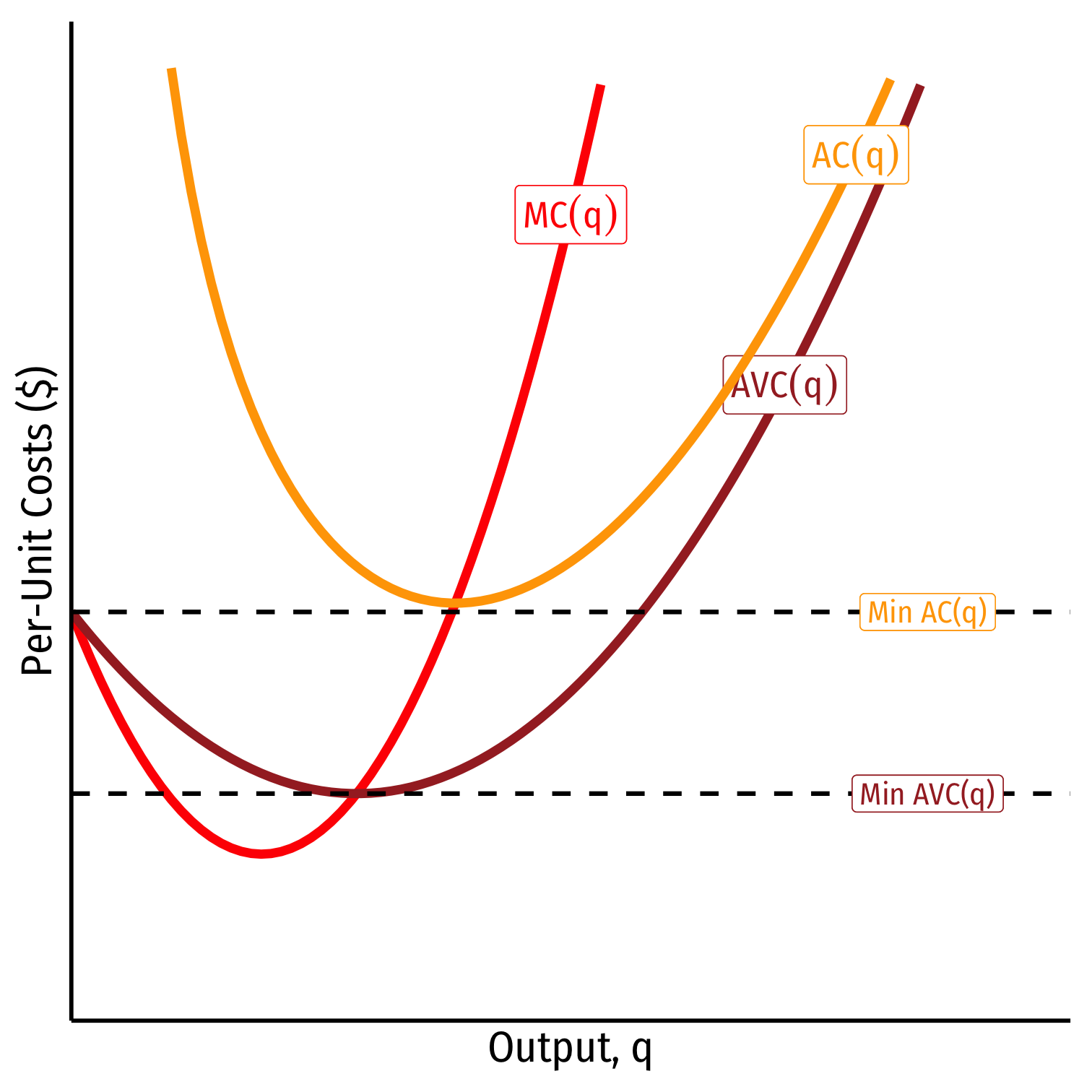

Relationship Between Marginal and Average

Relationship between a marginal and an average value:

marginal > average, average ↑

Relationship Between Marginal and Average

Relationship between a marginal and an average value:

marginal > average, average ↑

marginal < average, average ↓

Relationship Between Marginal and Average

Relationship between a marginal and an average value:

marginal > average, average ↑

marginal < average, average ↓

When marginal = average, average is maximized/minimized

- When MC=AC, AC is at a minimum

When MC=AVC, AVC is at a minimum

Economic importance (later): Break-even price and shut-down price

Costs: Example: Visualized

Costs in the Long Run

Long run: firm can change all factors of production & vary scale of production

Long run average cost, LRAC(q): cost per unit of output when the firm can change both l and k to make more q

Long run marginal cost, LRMC(q): change in long run total cost as the firm produce an additional unit of q (by changing both l and/or k)

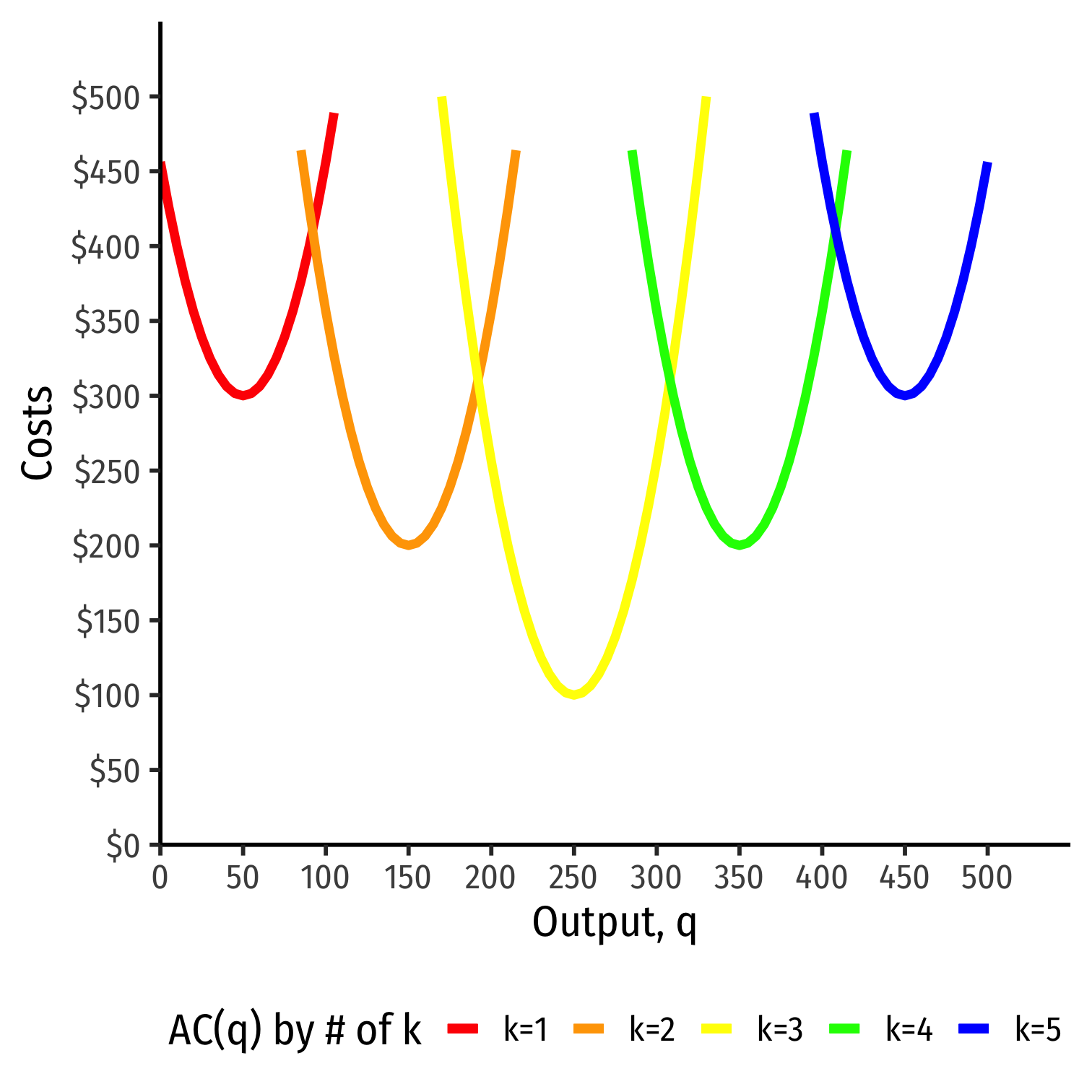

Average Cost in the Long Run

Long run: firm can choose k (factories, locations, etc)

Separate short run average cost (SRAC) curves for each amount of k potentially chosen

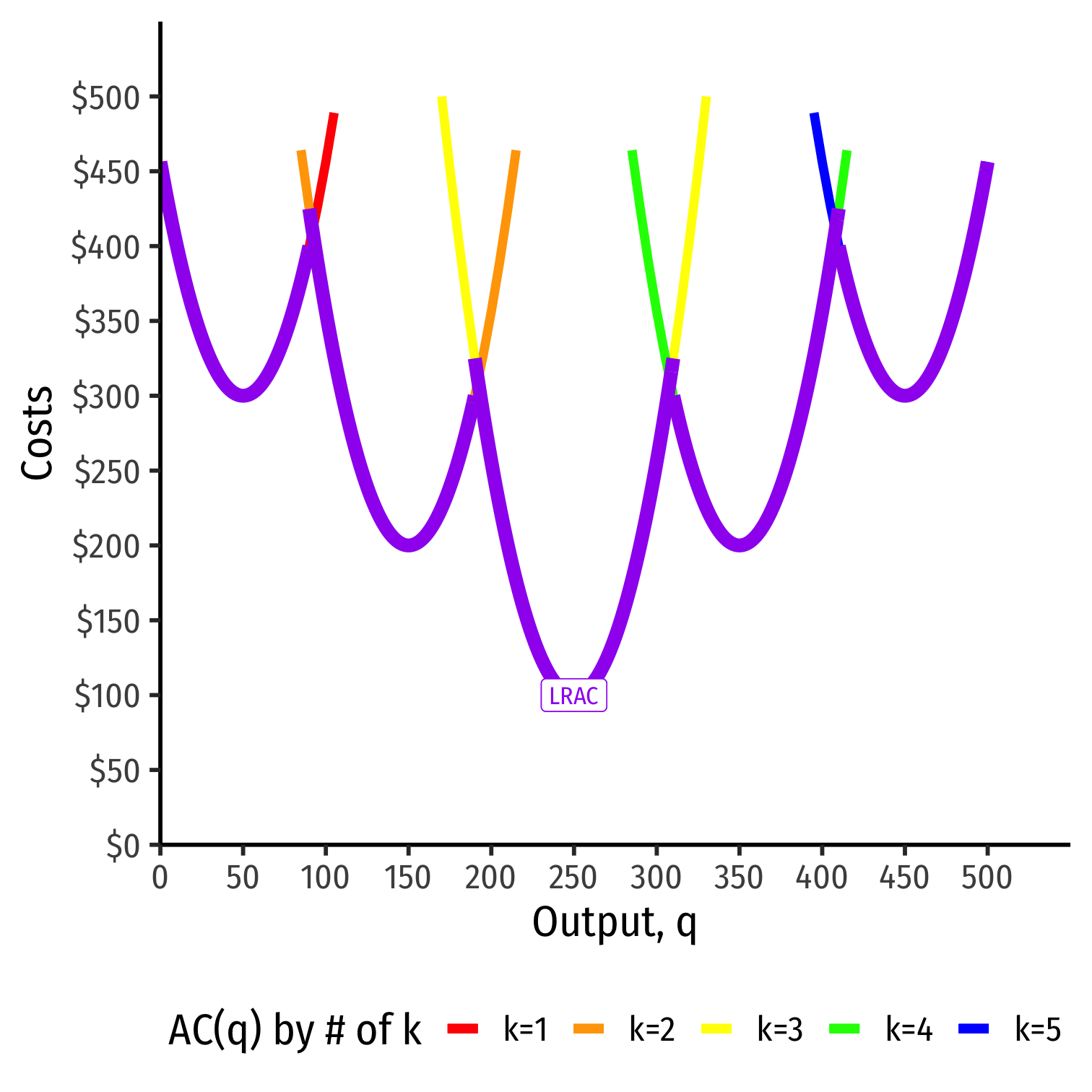

Average Cost in the Long Run

Long run: firm can choose k (factories, locations, etc)

Separate short run average cost (SRAC) curves for each amount of k potentially chosen

Long run average cost (LRAC) curve "envelopes" the lowest (optimal) parts of all the SRAC curves!

"Subject to producing the optimal amount of output, choose l and k to minimize cost"

Long Run Costs & Scale Economies I

Further properties about costs based on scale economies of production:

Economies of scale: costs fall with output

- AFC>AVC(q)

Diseconomies of scale: costs rise with output

- AFC<AVC(q)

Constant economies of scale: costs don't change with output

- Firm at minimum average cost

Long Run Costs & Scale Economies I

Note economies of scale ≠ returns to scale!

Returns to Scale (last class): a technological relationship between inputs & output

Economies of Scale (this class): an economic relationship between output and average costs

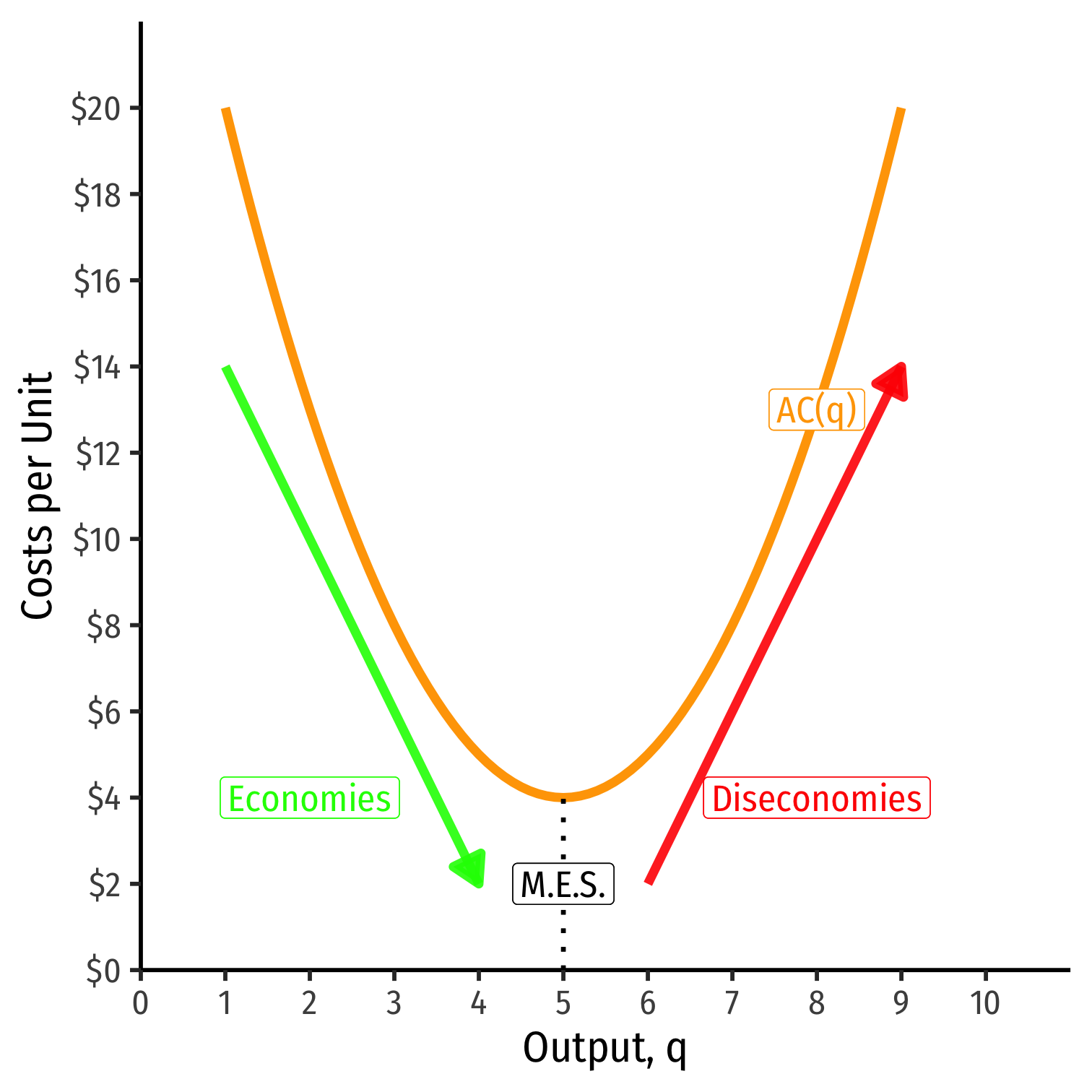

Long Run Costs & Scale Economies II

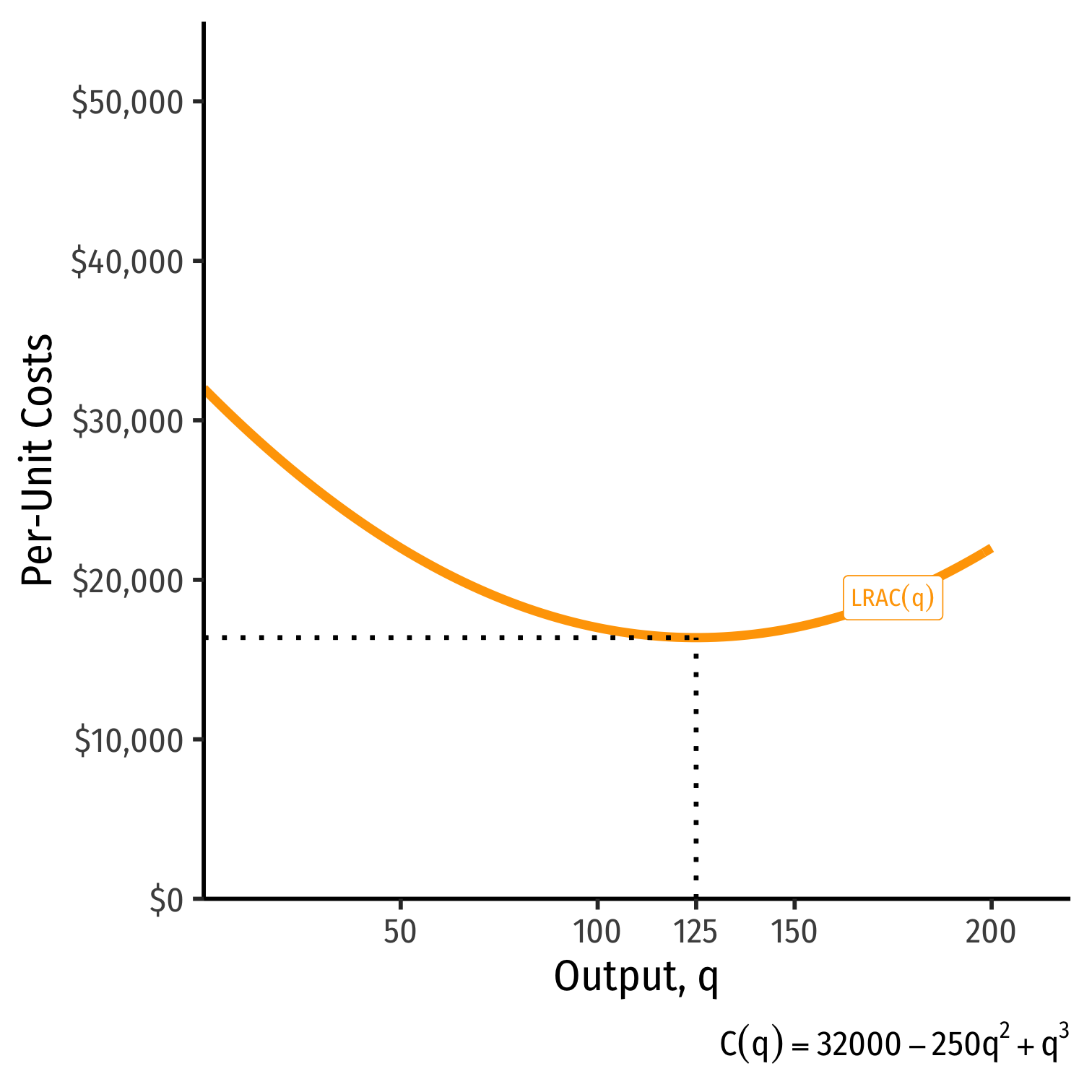

Minimum Efficient Scale: q with the lowest AC(q)

Economies of Scale: ↑q, ↓AC(q)

Diseconomies of Scale: ↑q, ↑AC(q)

Long Run Costs and Scale Economies: Example